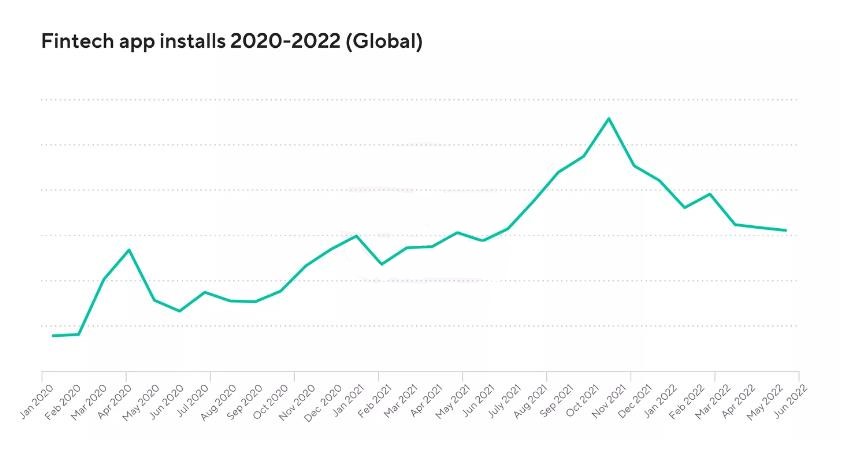

As previously cash-based businesses began to transition to digital payments in H1 2020, fintech app installs began to skyrocket. From February to March 2020, global fintech app installs increased by a whopping 26% month on month (MoM). After rebalancing, installs continued to rise, reaching an all-time high in November 2021. Installs were up 11% month on month in November 2021, and 32% higher than the monthly average in 2021.

This surge was primarily driven by the payment app sub-vertical in North America. Installs of payment apps increased by nearly 60% MoM in North America between October and November 2021. Over the years, Black Friday has grown in popularity as an e-commerce event, helping to cement November as the key time of year for e-commerce app marketers. Black Friday, Cyber Monday, and the associated month-long sales throughout November were most likely the primary cause of this rapid escalation, which was exacerbated by pandemic-related growth. While November was the best-performing month in 2020, YoY growth in November 2021 could reach 66%.

Installs fell slightly in Q2 2022, as consumers became more cautious about their spending as a global recession became more likely. However, by the end of H1, installs were up 4% year on year (YoY), indicating that we are still seeing an increase in fintech app installs this year.

Looking ahead to 2022, we can see that all sub-verticals are recovering after a dip at the start of the year. Even after the crypto crash in the middle of the year, we're seeing a recovery in installs. Similarly, after a difficult year in the stock market, data show that the tide is slowly turning toward a return to growth by August 2022.

With 473 FinTech unicorns worldwide, there are clearly numerous paths to success. What steps can you take to ensure yours? The following are some of the most important FinTech development trends for 2023.

Click "

Learn More" to drive your

apps & games business with the

ASO World app promotion service now.

1. 2023 FinTech Trends Web 3.0 and blockchain are being widely adopted for decentralization and security.

Despite the spectacular failure of non-fungible tokens (NFT) in many fields of digital entrepreneurship (including art and video games), many consumers are still interested in the concept of web 3.0. Implementing blockchain, artificial intelligence (AI), and machine learning allow for the creation of a completely new level of customer experience. This can and is a top FinTech trend when combined with new services.

Biometric measures will be used by FinTech companies to confirm and secure payments. This will add an extra layer of security to bank accounts, ATM transactions, payment apps, credit and debit cards, and so on. Biometry is already used by companies such as Hypr, Keyless.io, and Transmit. They also incorporate various use cases to ensure that the solution runs smoothly.

2. Digital-only banking is imminent.

There is no need to visit any brick-and-mortar bank, no lines to test your patience, and no agonizing paperwork to deal with, so digital-only banks have a lot going for them. And their numbers and revenue are increasing all over the world (Global Market Insights, 2019). They're also one of the main reasons why bank branch visits are expected to fall 36% between 2017 and 2022. (The Financial Brand, 2021).

When you use digital-only banks, you can also reset pins from the comfort of your own home, make snap-a-pic bill payments, access convenient expense management tools and quick balance review features, and get real-time analytics.

However, don't rush to sign up for any of these fintech disruptors. Consider that, like any other business, they are bound to be prime targets of the financial fraudsters lurking all over the internet. This should weigh heavily on your decision in an age when financial fraud is the leading internet crime worldwide.

3. Artificial intelligence and machine learning benefit the entire industry.

AI improves business operations by detecting fraud, scanning potential security threats, and more. Companies and customers can both benefit from improved risk management, lower operating costs, personalization of banking experiences, and automated workflows.

FinTech development trends in 2023 point to AI as one of the major factors driving the industry's future growth. The Royal Bank of Canada, for example, uses AI to improve user experience and deliver new applications to customers more quickly. RBC's private AI cloud can analyze millions of data points per second, allowing a company to build and deploy AI-powered apps more efficiently.

The first true digital natives, Gen Zers, will also play an important role in the discussion of payment innovations. As it is, they are the first generation to experience cashless transactions and are thus more familiar with these innovations.

* Grow with our app growth solutions - choose a

guaranteed app ranking service for the

TOP 5 app ranking acquirement, and maximize your app traffic. Or click the "

Promote Now" above (to

increase app installs service for app visibility).

*

What Is the Keyword Guaranteed Ranking Service? What Is the Advantage of It?

4. Payment innovations

Fintech payment innovations include a variety of components. Mobile payments, contactless payments, mobile wallets, smart speaker systems, identity verification technologies, AI, and machine learning are examples of security technologies.

According to 2020 figures, the most significant trend in payment innovations is the rise of mobile payments, particularly during the COVID-19 pandemic, when more transactions shifted online (PaymentsJournal, 2020). Mobile payments, however, do not only cover online purchases. In-store transactions are expected to exceed 2.7 billion by 2022, bringing the total value of global e-commerce transactions to more than $5.4 trillion by 2025. (Payvision, 2020).

5. An increased emphasis on exploring new business avenues. Even if that means collaborating with competitors.

Goldman Sachs recently did this with Elinvar, gaining a stake in the digital banking space (Finextra Research, 2019). Goldman Sachs is not alone in this regard. Visa also launched an investment fund for fintech startups, which is expected to bolster Visa's position in the digital banking market (MarketWatch, 2020).

These are relatively new and well-documented collaborations. They will abound in the future. FinTechs do not always have the funds or infrastructure to handle their customers' operations. Banks, as previously understood, are not always quick and astute enough to respond to rapidly changing market conditions. FinTechs can help with this. We anticipate increased collaboration in the coming years.

Conclusion

FinTech development trends for 2023 demonstrate that digitalizing what is already digital is not a strange statement. Mobile app development, and more broadly, FinTech development, necessitate a new and fresh point of view.

COVID-19 UPDATE

COVID-19 UPDATE