COVID-19 UPDATE

COVID-19 UPDATE

Important Notice:Beware of scams using ASOWorld's name for part-time recruitment or ASO earning app activities. ASOWorld is not hiring any part-time staff. Trust only official information posted by ASOWorld.

Objective analysis of the global esports sector up to 2026. Examine market valuations, audience demographics, segment growth, actionable mobile game marketing strategies.

Riot Games, the developer of League of Legends (LoL), introduced a structurally adjusted business model for esports in 2024. This model features a Global Revenue Pool (GRP) designed to distribute revenue generated from digital LoL esports assets.

This operational framework applies to franchises within the North America-based League Championship Series (LCS), the League of Legends European Championship (LEC), and the League of Legends Champions Korea (LCK).

This structural shift was implemented to mitigate reliance on brand sponsorships following post-pandemic economic adjustments. Riot pledged a 50% revenue share after recovering operational esports investments and continues to coordinate with China's LPL to standardise this model globally.

※ Strategic Observation: Transitioning from an exclusively sponsor-dependent model to one weighted towards digital sales provides enhanced economic resilience. Digital content distribution offers scalable revenue without the contractual friction or volatility associated with traditional sponsorship terms.

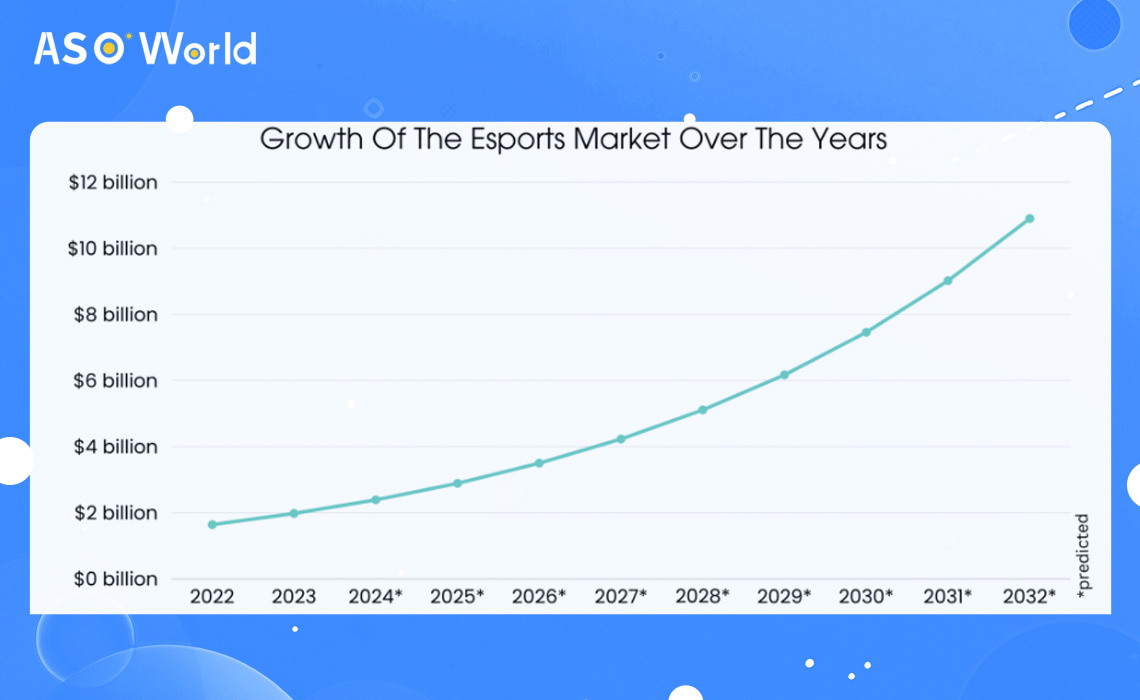

The global esports ecosystem was valued at $1.98 billion in 2023. Driven by a compound annual growth rate (CAGR) of 20.9%, the sector reached an estimated $2.39 billion by the end of 2024. Current projection models indicate that the market value is structurally positioned to hit $10.9 billion by 2032.

The United States maintains a dominant position concerning gross revenue. The US sector, valued at approximately $871 million in 2023, exceeded the $1.07 billion mark in 2024. With a forecasted CAGR of 18.7% progressing towards 2028, the US market is expected to reach $1.51 billion. Concurrently, the UK and broader European markets have demonstrated steady consolidation, largely driven by integrated telecom partnerships and an established mobile consumption base.

Sponsorship remains a critical revenue channel. Historical data from 2022 indicates that esports sponsorship revenue exceeded $837.2 million. Media rights and publisher fees collectively generated an estimated $338.5 million, highlighting the ongoing necessity of diversified IP monetisation.

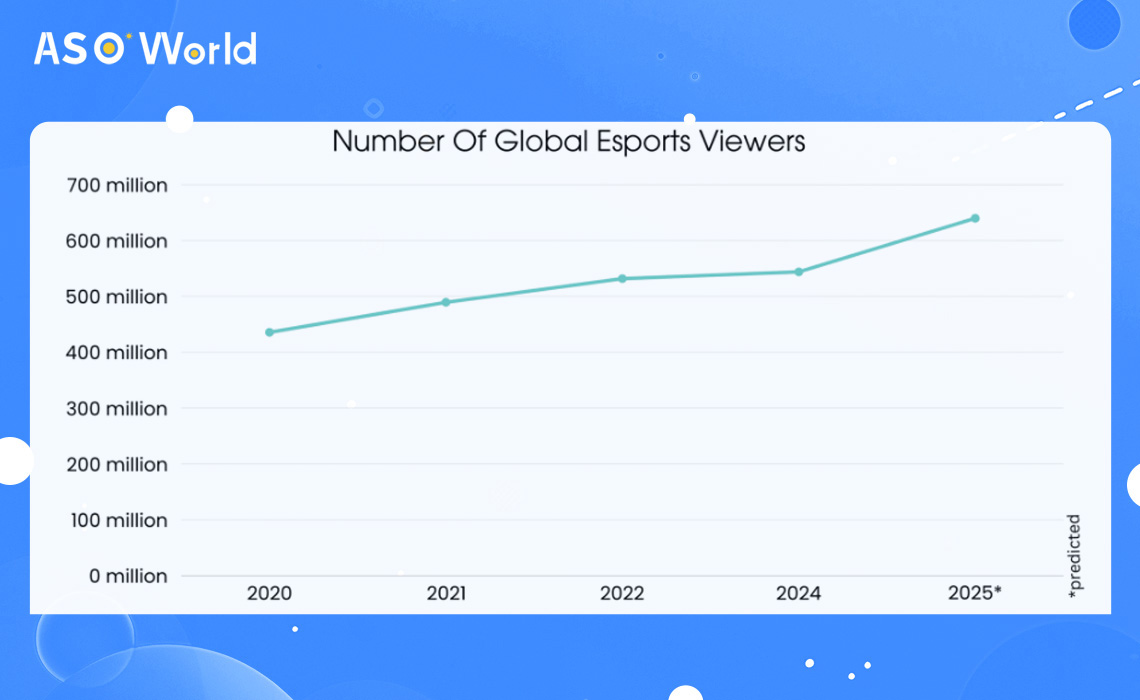

Facilitated by the globalisation of mobile gaming and innovations in broadcasting protocols, viewership has scaled predictably. Total global viewership escalated from 435 million in 2020 to over 540 million in 2024. By 2025, the aggregated global audience successfully surpassed 640 million viewers as the medium matured into conventional broadcasting channels.

As the demographic ages and integrates into mainstream media consumption, user retention within esports ecosystems has stabilised. In 2022, the active demographic comprised 261.2 million enthusiasts and 270.9 million occasional viewers. By the conclusion of 2025, these figures evolved, with occasional viewers exceeding 322.5 million and core esports enthusiasts surpassing 318.1 million globally.

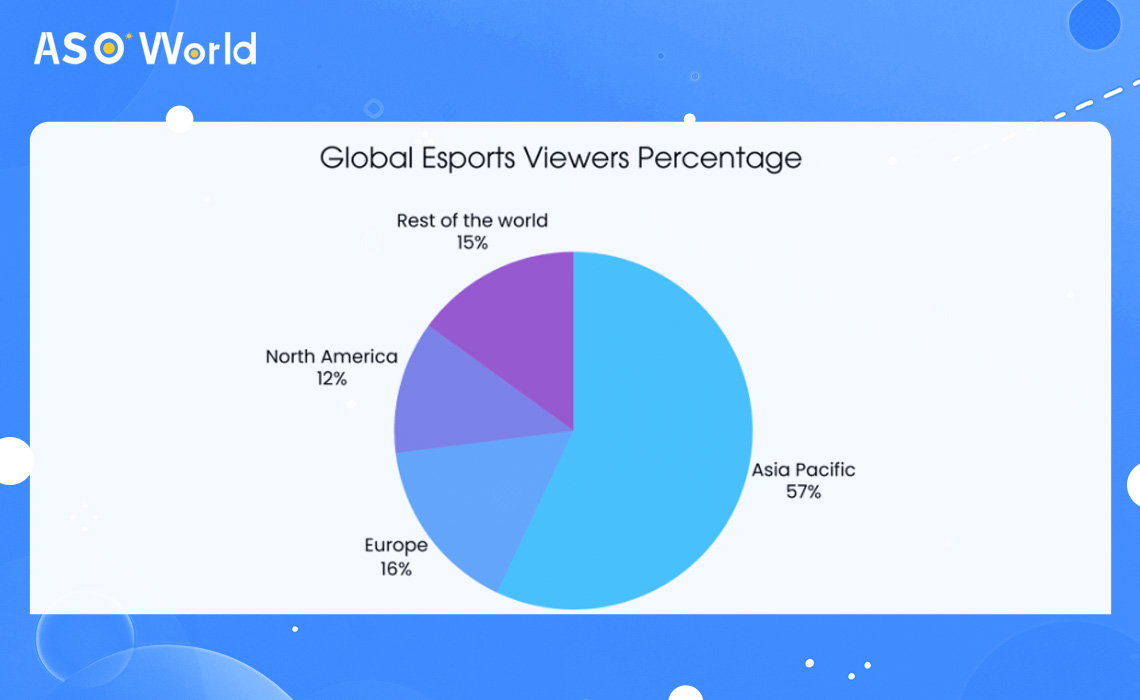

With an active gaming population exceeding 1.5 billion, the Asia-Pacific (APAC) region contributes the demographic majority of esports viewership. Markets such as China and Indonesia maintain a high viewing rate (57%), claiming the largest single share of global audiences.

In comparative terms, the US base measured approximately 45 million in 2023, while the European market, including the UK, accounts for roughly 16% of the overall global viewer distribution.

The advertising segment maintains a primary share of market revenue. In-game ad placements enable targeted reach across specific demographic quartiles, increasing Cost Per Mille (CPM) rates. Furthermore, naturalised integration within live esports broadcasts results in higher brand retention metrics compared to traditional programmatic mobile advertising.

Sponsorship operations continue to yield stable financial growth. Evaluating the sector analytically, sponsoring endemic and non-endemic brands correlates directly with lifetime value (LTV) increases among loyal fanbases. The digitisation of assets by major publishers has formalised the procurement process for agencies looking to target the esports demographic.

Multiplayer Online Battle Arenas (MOBAs) command a disproportionate share of current market engagement, driven by high-fidelity mechanics in titles such as "League of Legends" and "PUBG Mobile." The genre's systemic requirement for team coordination naturally translates to high-yield competitive broadcasting.

Additionally, the fighting game sector shows consistent single-digit growth trajectories, supported by the integration of modern netcode protocols ensuring stable cross-regional match matching.

⚡ MOBA Game Case Study: Global Market Expansion via App Localisation

Market expansion in North America and the UK is underpinned by near-ubiquitous fibre-optic broadband penetration. Integration of esports frameworks into secondary and tertiary educational institutions (via university esports programmes) provides a structured talent pipeline and localises community engagement.

The APAC region remains the foundational hub of mobile esports. Substantial increases in mobile hardware adoption across South Korea, Japan, China, and India define this sector. Furthermore, 5G infrastructure scaling in emerging markets like Vietnam, Thailand, and the Philippines directly reduces latency bottlenecks, raising the operational standard for competitive mobile gaming.

A subsidiary of Activision Blizzard (now operating under Microsoft), this California-headquartered organisation manages intellectual properties such as "Call of Duty." It holds a fundamental position in cross-platform competitive operations.

Established in 1982, EA manages premier sports simulation franchises like "FIFA" (now "EA Sports FC") and "Madden," alongside action properties. EA leverages consistent annual release schedules to maintain a cyclical competitive calendar.

Constructed around the mobile ecosystem and headquartered in Paris, Gameloft focuses on maintaining substantial monthly active user (MAU) bases across portable devices, bridging the gap between casual and competitive networking.

The landscape includes strategic corporate involvement from Tencent Holdings Limited, Skillz Inc., Gfinity PLC, Riot Games, Inc., and CAPCOM Co., Ltd., each operating discrete segments of the hardware, software, and event management verticals.

>>> For baseline 2023 metrics, view the historical archive 👉 Retrospective: Global esports Market Report (2023)

Access to 5G and high-bandwidth broadband globally acts as an infrastructure prerequisite for sector growth. Cloud gaming architectures similarly lower the hardware barrier to entry, normalising user acquisition costs across both established and emerging economies.

Uninterrupted, low-latency data packaging allows for high-bitrate streaming of competitive events, fulfilling the baseline technical requirements needed to sustain an audience accustomed to modern broadcast standards.

The operational shift towards mobile esports continues to capture the highest volume of new users. Current hardware specifications on mid-to-high-tier smartphones meet the processing requirements for competitive frame rates.

Publishers have correspondingly adapted development protocols to prioritise touch-interface optimisation, ensuring the final software product is native to the platform rather than a rudimentary port.

※ Executing Actionable Mobile App Optimisation:

Marketing competitive mobile titles requires adherence to strict User Acquisition (UA) and App Store Optimisation (ASO) strategies. In practical terms, executing A/B testing on store assets (e.g., visualising in-game UI layouts and competitive rankings in screenshots) directly correlates with increased App Store conversion rates. Incorporating local dialects and regional tournament nomenclature within the keyword metadata targets high-intent search traffic efficiently.

Monetisation through hybrid models (freemium installation supplemented by cosmetic Battle Passes) provides operational liquidity. Aligning UA campaign spend with local esports event calendars significantly mitigates CPI (Cost Per Install) inflation.

Traditional sporting groups consistently operate parallel esports divisions to capture younger digital demographics. The entry of premier football, racing, and basketball clubs formalises market structures and aggregates external capital into the sector. This also enables cross-promotional marketing channels, transferring traditional sporting audiences towards digital viewing habits.

Governmental frameworks targeting the legalisation and regulation of esports betting actively inject measurable capital into the ecosystem. The existence of state-level oversight mitigates algorithmic fraud, ensures operational transparency, and provides a safer environment for consumer participation. Regulated markets command higher investment confidence and attract rigorous institutional capital.

South Korea operates as a mature testing environment for macro esports implementation due to its saturated gaming infrastructure and ingrained socio-digital habits. State support for municipal stadium construction and local league cultivation sustains an exceptionally active domestic market.

The existence of PC Bangs (LAN gaming centres) functions as a decentralised community network, maintaining active player loops and accelerating the adoption rate of competitive properties.

※ Execution Strategy: To secure market penetration in regions with high competitive densities like South Korea or the UK, mobile developers must execute highly localised promotional frameworks. Off-line partnerships with regional telecom providers and physical gaming spaces yield positive brand-association metrics.

Executing strategic placement within region-specific app stores and optimising the application’s search visibility remains an absolute requirement.

ASOWorld continuously publishes objective technical blueprints for distinct geopolitical markets. Adjust your operational roadmap with our data.

Click " Register and Learn More" to scale your developmental operations via the quantitative ASO World mobile app promotion services tier today.

Generative Artificial Intelligence and blockchain architecture serve as functional utilities rather than speculative concepts within modern esports protocols. Analytical AI models compute real-time statistical probabilities during broadcasts, providing data-centric engagement for audiences. Machine learning algorithms concurrently analyse background processes to enforce anti-cheat guidelines, preserving mechanical integrity.

Blockchain integration is chiefly utilised for establishing verifiable digital scarcity of in-game cosmetic assets. Cryptographically secured fan tokens allow franchise operators to quantify user loyalty and implement voting systems for low-stakes administrative decisions.

⚡ Industry Insights: Generative AI in Game Development

Upon reviewing the operational period leading up to 2026, the global esports economy acts as a highly integrated subset of the wider digital entertainment sector. Sustained audience scaling, codified revenue-sharing models, and targeted technical implementations (5G latency reduction, AI analytics) define the current phase of the industry.

For developers and agencies seeking logical pathways to deploy digital properties within this competitive environment, maintaining structural compliance with active market trends is essential. Access further operative tools via ASOWorld.

Mobile App Growth,Mobile Insights,

Mobile App Growth,Mobile Insights,

Get FREE Optimization Consultation

Let's Grow Your App & Get Massive Traffic!

All content, layout and frame code of all ASOWorld blog sections belong to the original content and technical team, all reproduction and references need to indicate the source and link in the obvious position, otherwise legal responsibility will be pursued.